The first step in buying a home is to get a prequalification letter from a lender.

During the prequalification process, you’ll fill out an application and provide documents to verify your financial information. Then the lender will look at your income, assets, and credit score to estimate how much you can borrow.

A prequalification is a quicker and more informal version of a preapproval.

Here are the steps to get a prequalification letter.

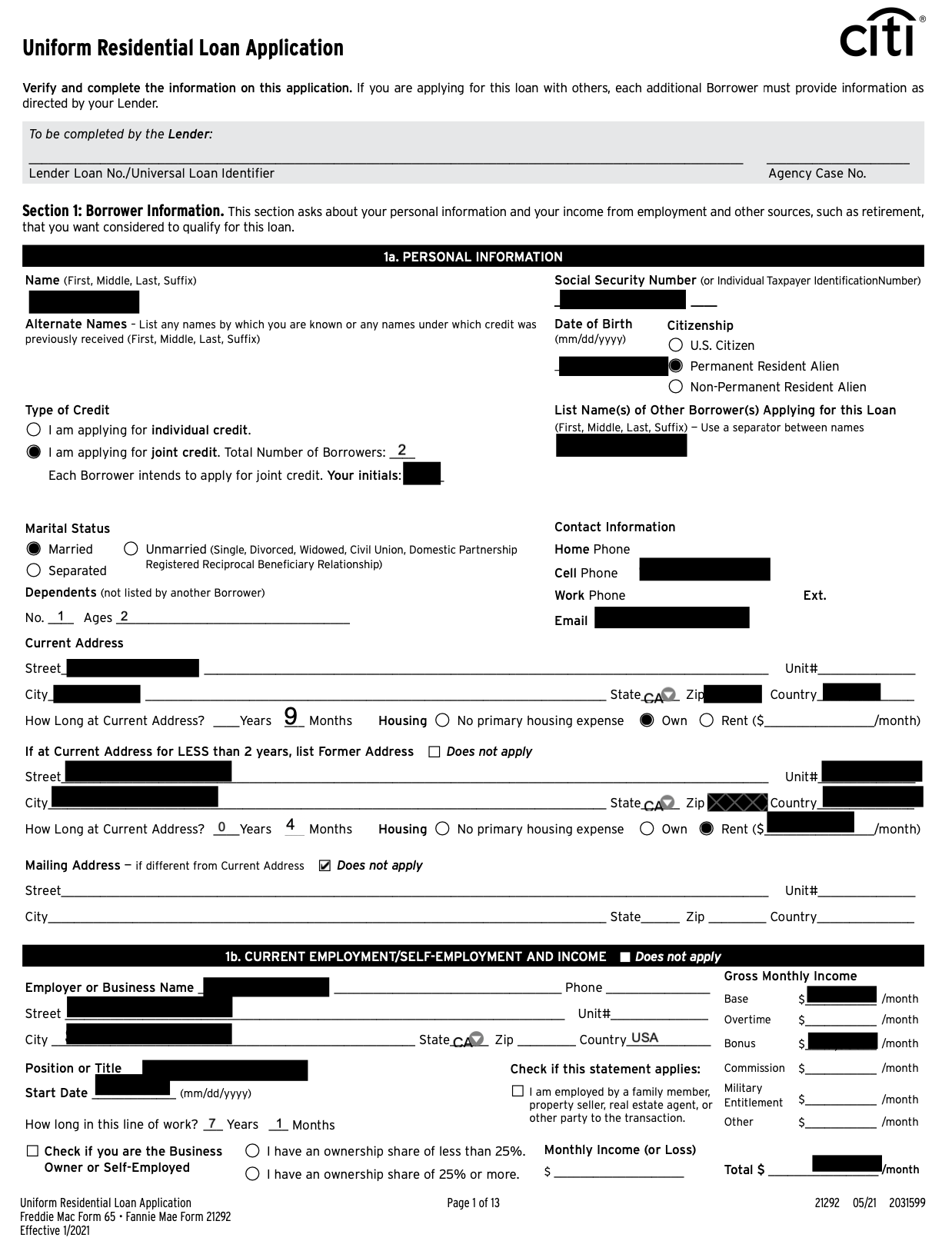

First, reach out to a lender and get a copy of the loan application.

Here are some tips for putting your best foot forward when filling out the application.

This is the first page of the loan application I filled out last year.

In addition to answering questions in the application, you also have to provide supporting documents to prove your income (W2) and assets (bank statements).

These are the supporting document I had to provide:

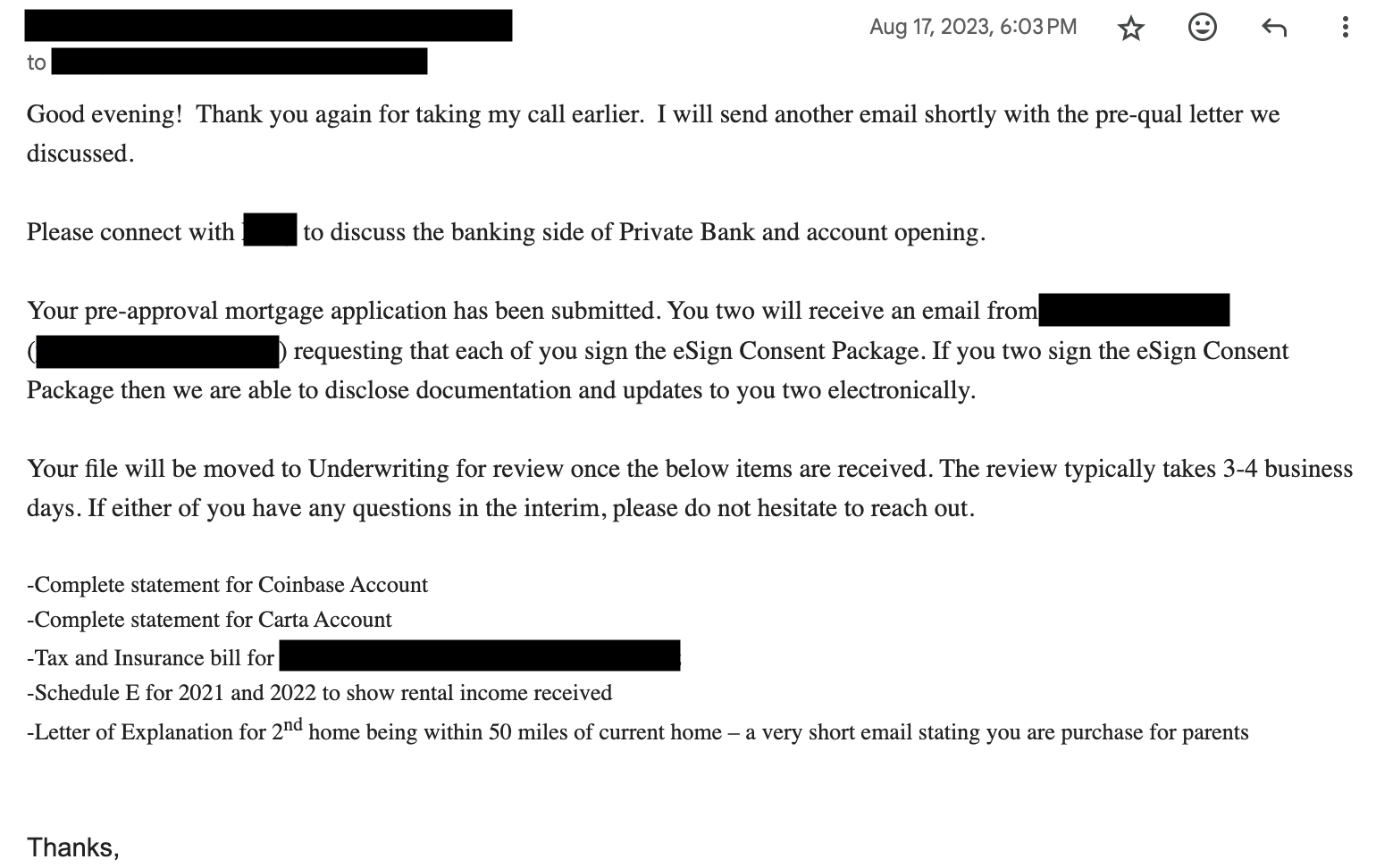

After you have submitted the application, you might receive additional questions or document requests.

Here is the email I got from the bank. We got the prequalification letter but the lender wanted us to get a head start on the full loan approval, so they asked for follow-up docs.

Next, the lender will give you an estimate of the amount they are willing to lend you.

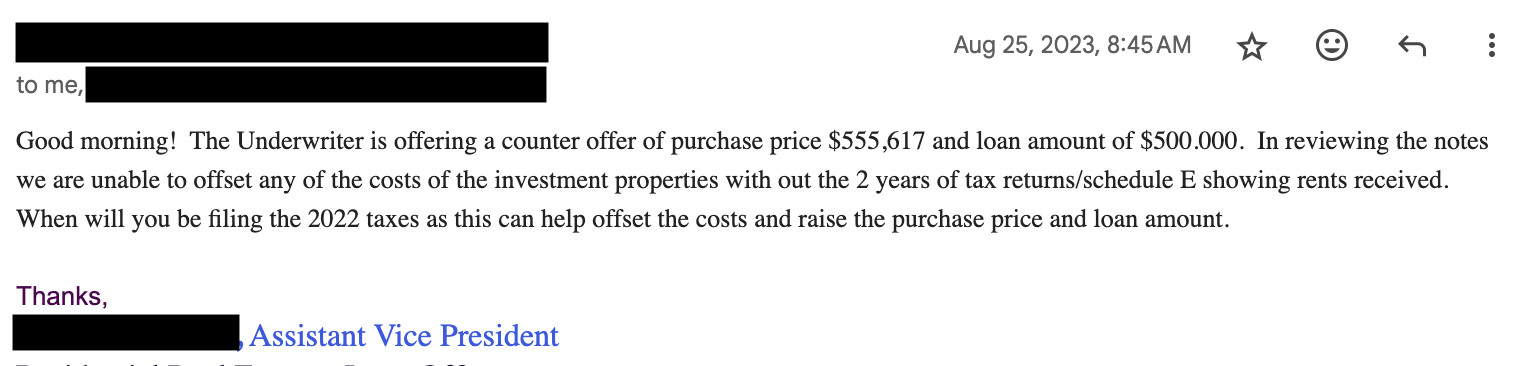

In my case, I wanted to borrow more but the bank was only willing to lend $500k.

They said it was because I had just started renting out our old NJ home, I hadn't filed a tax return showing that income yet, so none of that income could be included in the application. 😢

If you are relying on other sources of income to boost your application, they have to be listed on your tax return. Otherwise, they won't count.

Once you have found a home you want to bid on, ask for a prequalification letter in the exact amount you plan to borrow.

Showing a prequalication letter for more than you need reveals to the seller that you can pay more.

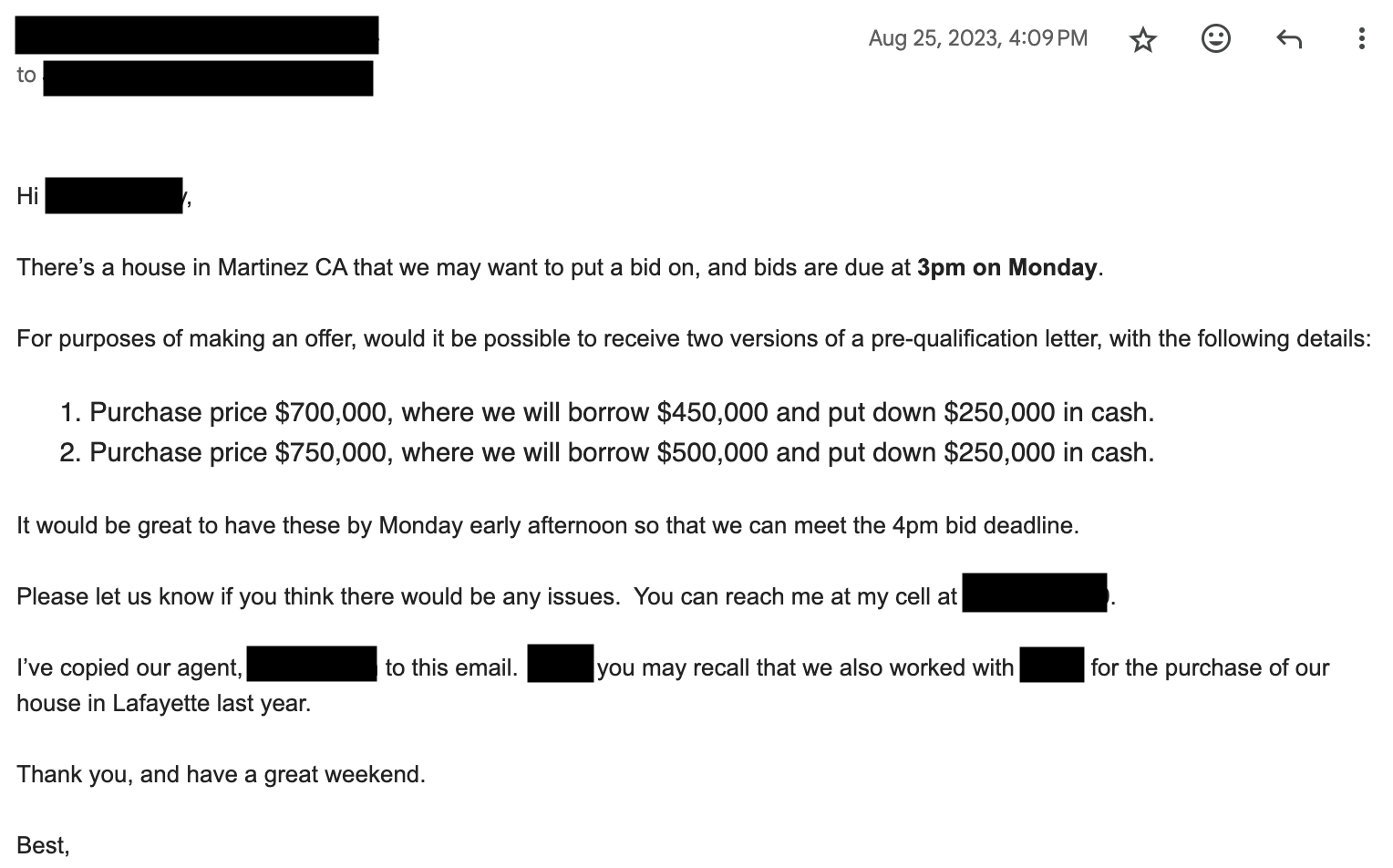

Here is how I asked for the prequalification letter.

I wasn't sure exactly how much I wanted to bid, so I asked for pre-approval letters with a couple different amounts.

After going to open houses over the weekend, if you find a house that you want to put a bid on, send an email to the lender first thing on Monday morning.

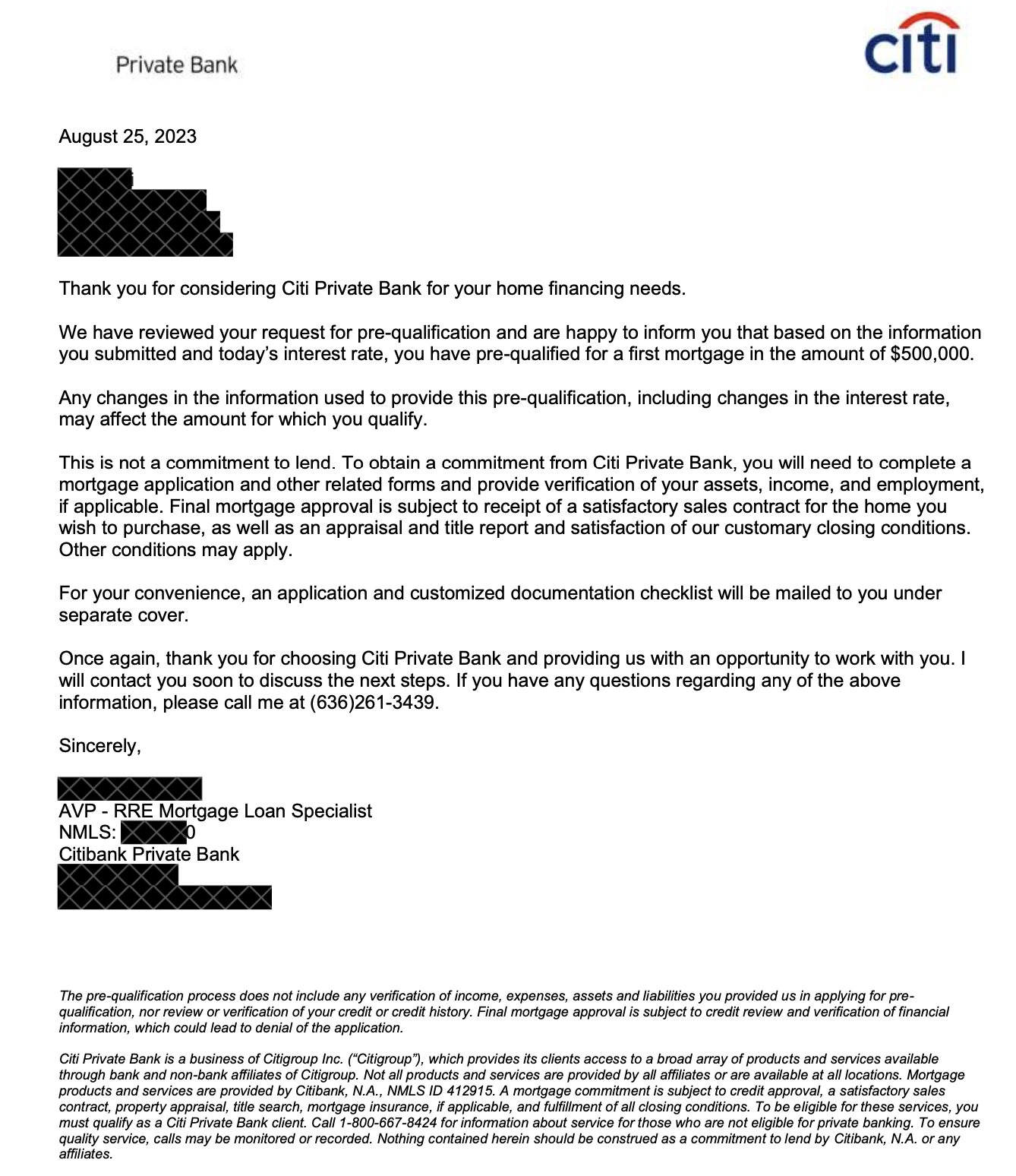

This is the actual document we received from the bank and used to submit the bid for the property.

Double check that the loan amount is correct and that it is dated as of the day you are submitting the bid.

The date proves that your prequalification isn't out of date.