If you're planning to buy a home, you're going to need to sign a residential purchase agreement. The good thing is that the seller's real estate agent can provide the standard residential purchase agreement, but you still need to understand the key terms.

Chances are you don't have time to become a contract law expert and parse through the legalese. As a former lawyer who has purchased 4 houses, I can help you understand how the residential purchase agreement works.

This is a ranking of the top 10 terms in the actual residential purchase agreement I used last year. Let's take it from the top, starting with purchase price.

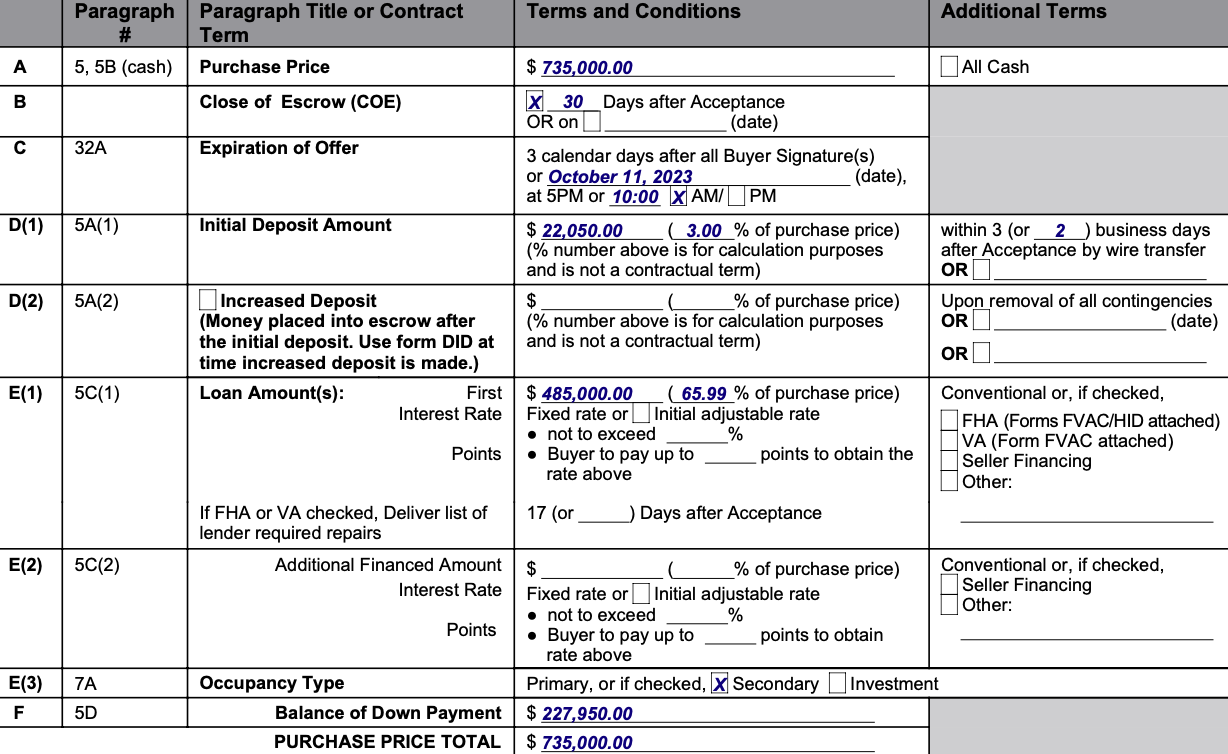

Purchase Price is the total amount of money agreed upon for the sale of the property. This includes the Loan Amount, which is the amount you plan to finance with a mortgage, and the Down Payment, cash you wire on the day of closing.

This is the key part of the residential purchase agreement I actually used last year.

An escrow is an account controlled by a trusted third party, the escrow agent, which holds your initial earnest money deposit and transfers it to the seller on the day of closing.

Initial Deposit (aka Earnest Money) is the amount of money you must transfer to the escrow agent within 3 days of an accepted offer. This is called "opening the escrow account." The deposit counts towards your down payment and is a signal that you are a serious buyer.

Close of escrow is the date you officially become the owner of the property. What happens is that the escrow agent transfers the money in the escrow account to the seller and officially closes the account. Typically this is 30 days after your offer is accepted.

Liquidated Damages means that if you break the contract, the seller will keep your initial deposit as a penalty. 😱

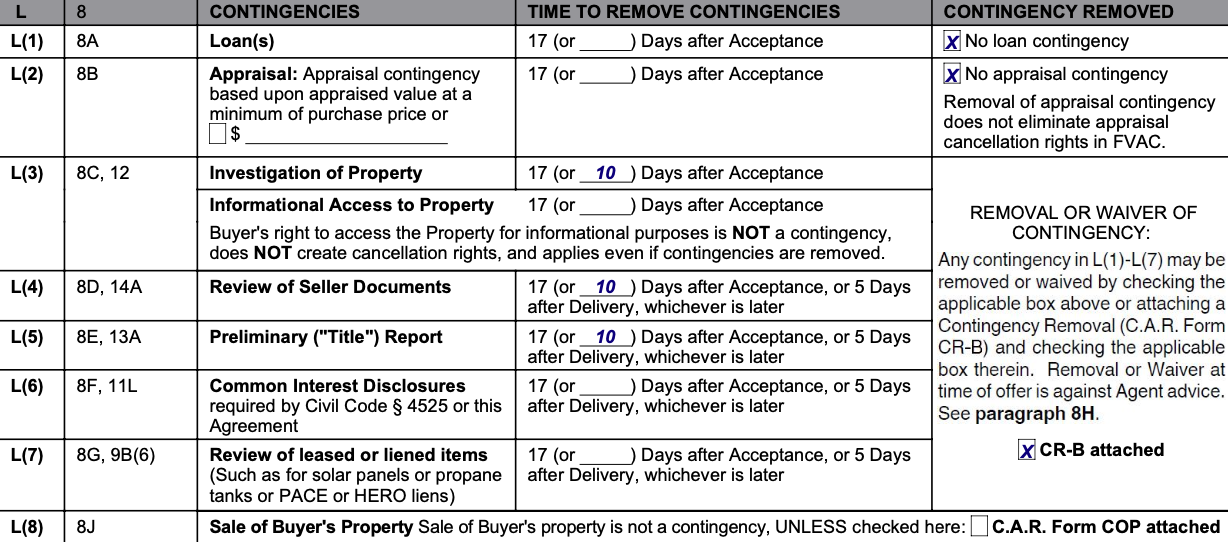

A contingency is a requirement that must be satisfied before the sale can be completed. If a contingency is not met, the buyer can cancel the contract without penalty.

Contingencies are a buyer's best friend. They give you a right to terminate the contract for certain legitimate reasons. We'll get into the specific reasons below.

First, this is how the contingency process helps buyers:

Here are the contingencies from the actual contract we signed last year to purchase a house. We removed the loan and appraisal contingencies because we were confident we would get financing. This is one tactic to make your bid stronger, but I don't recommend it for first time buyers.

Loan contingency makes your obligation to purchase the property dependent on obtaining mortgage financing. This protects you by allowing you to back out of a deal if you are unable to secure a loan.

17 days is the default deadline for you to get your loan approved by the bank. After signing the contract, reach out to your lender to make sure they have everything they need to approve the loan.

Appraisal contingency makes your obligation to purchase the property dependent on the property being appraised at a value equal to or higher than the agreed-upon purchase price. This protects you and the mortgage lender by ensuring that you are not overpaying for the property.

17 days is the default deadline for you to get your appraisal contigency. You don't have to do much here because typically your lender will order an appraisal report from a licensed appraiser.

Investigation of property is a contingency that allows you to conduct various inspections of the property before finalizing the purchase. This protects you by giving you an opportunity to identify any deal-breaker issues that would cause you to cancel the contract.

Unless you are an expert in home inspections, I recommend hiring for experts to do inspections:

17 days is the default deadline for you to get inspection reports, get quotes for repairs, and decide whether to request repairs or request a lower purchase price. It's a lot to do by the deadline, so order your inspections as soon as possible after you have a signed contract.

Review of seller documents allows you to review various disclosures by the seller before committing to the purchase. This gives you the chance to ensure all information is disclosed and ask any follow-up questions about the property.

Here are some common disclosures to look for:

In many states, sellers are actually required to complete a Transfer Disclosure Statement (TDS). The TDS discloses known defects or issues with the property that may impact its value, including structural, electrical, and plumbing issues.

Preliminary title report is a contingency that allows you to review the title report before finalizing the purchase. This is something the seller's agent, escrow agent, or title company will provide.

Here are some issues to watch for when reviewing a preliminary title report:

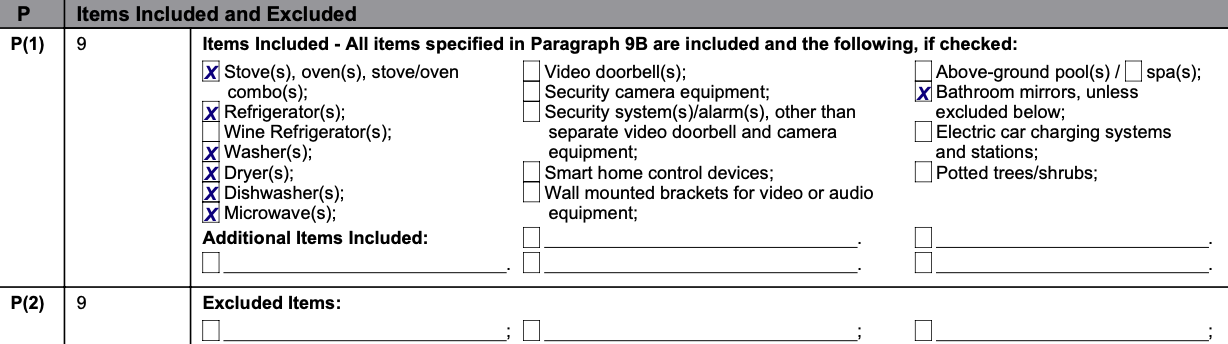

Items included and excluded lays out exactly what is and is not part of the purchase. Here are items typically included:

These are items usually excluded:

We've listed the standard items, but you can always negotiate for something different. For example, the buyer might want to keep a special hot tub, portable shed or chandelier.

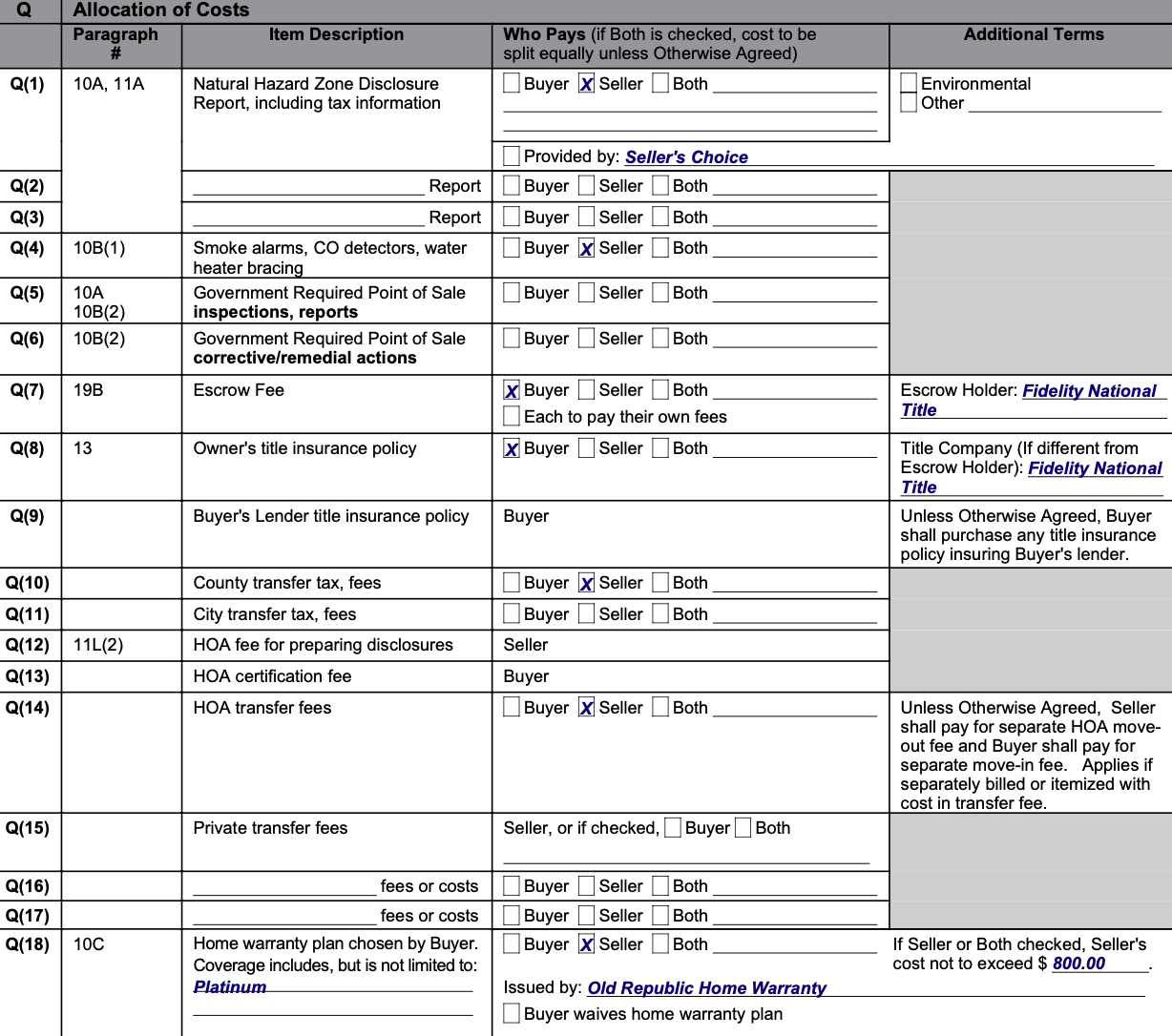

Allocation of costs clarifies who will be responsible for paying various expenses associate with the transaction. Here are the costs typically paid by the seller:

These are costs typically paid by the buyer:

This is the actual allocation of costs for a house I bought last year.