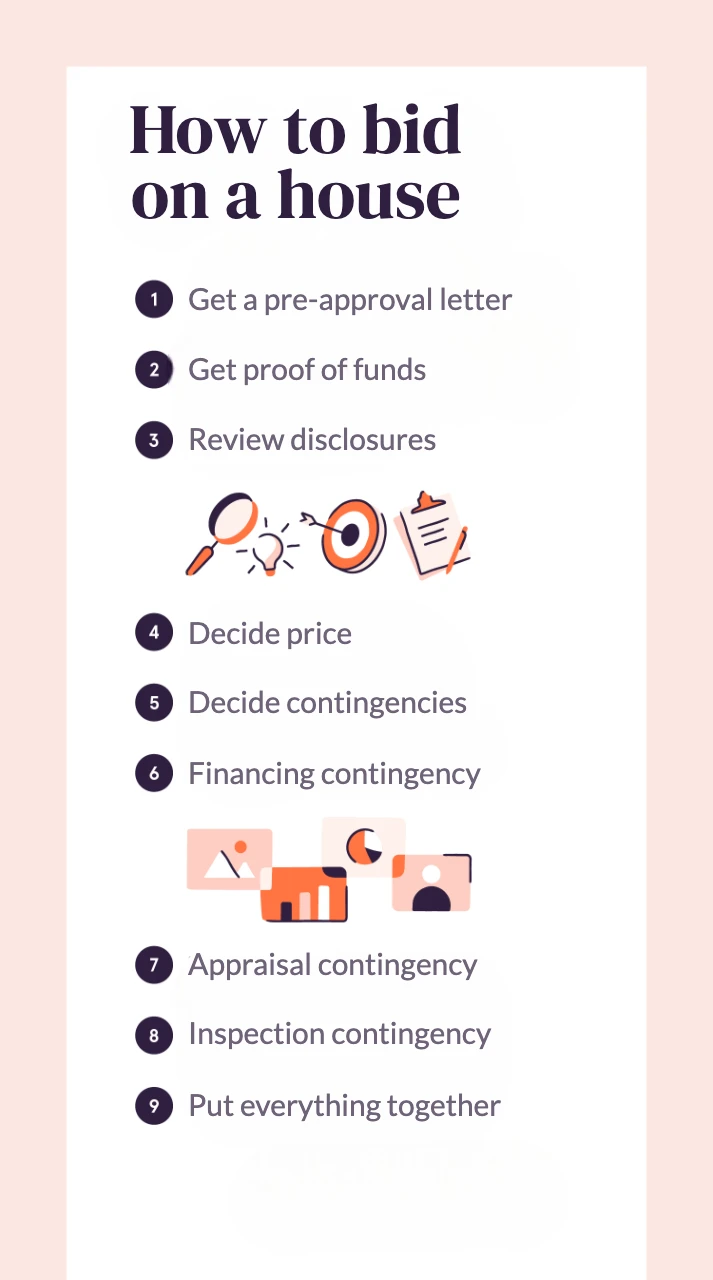

To make sure your bids hit the mark, we’ve rounded up the 6 steps to buy that home.

Let's take it from the top.

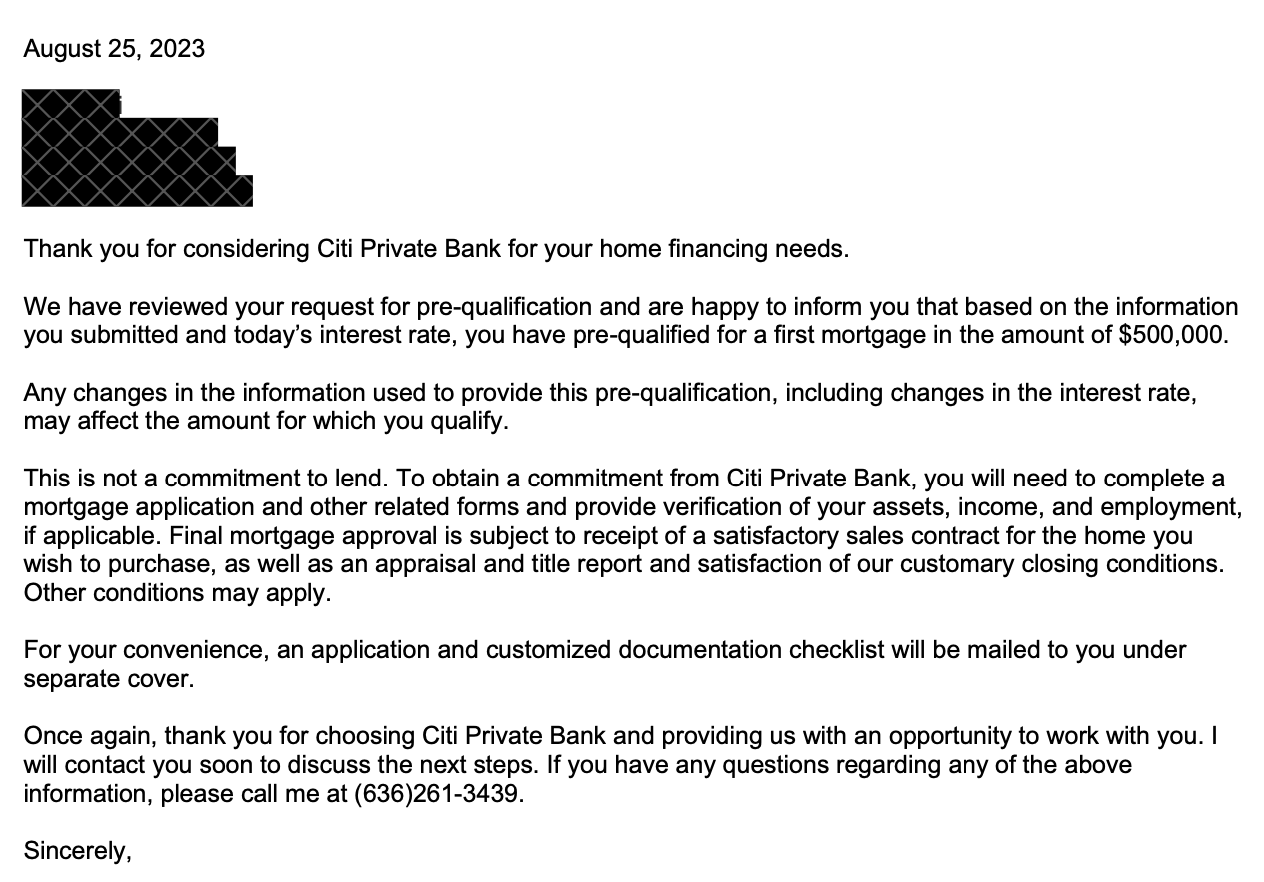

Getting a prequalification letter is typically the first step when you want to get serious about buying a home.

After you have given a lender some initial financial information, you will get a prequalification letter with an estimate of how much money you can borrow to buy a house.

This proves to the seller that you have already passed an initial review by the lender and the lender is willing to “prequalify” you for a mortgage up to a certain amount.

This is an actual pre-qualification letter that I received. Here, the lender is willing to prequalify me for a mortgage in the amount of $500,000.

The estimated mortgage amount can change based on interest rates. For example, we got this letter in August but by the time we found a house in October, interest rates had gone up and the lender was only willing to lend us $450,000.

Next, you can start calculating the amount of down payment you want to make. A down payment is cash you will pay for the house on the day of closing.

Down payments can range between 3 percent and 20 percent of the purchase price, depending on the type of mortgage used. Some loan programs don’t require a down payment at all.

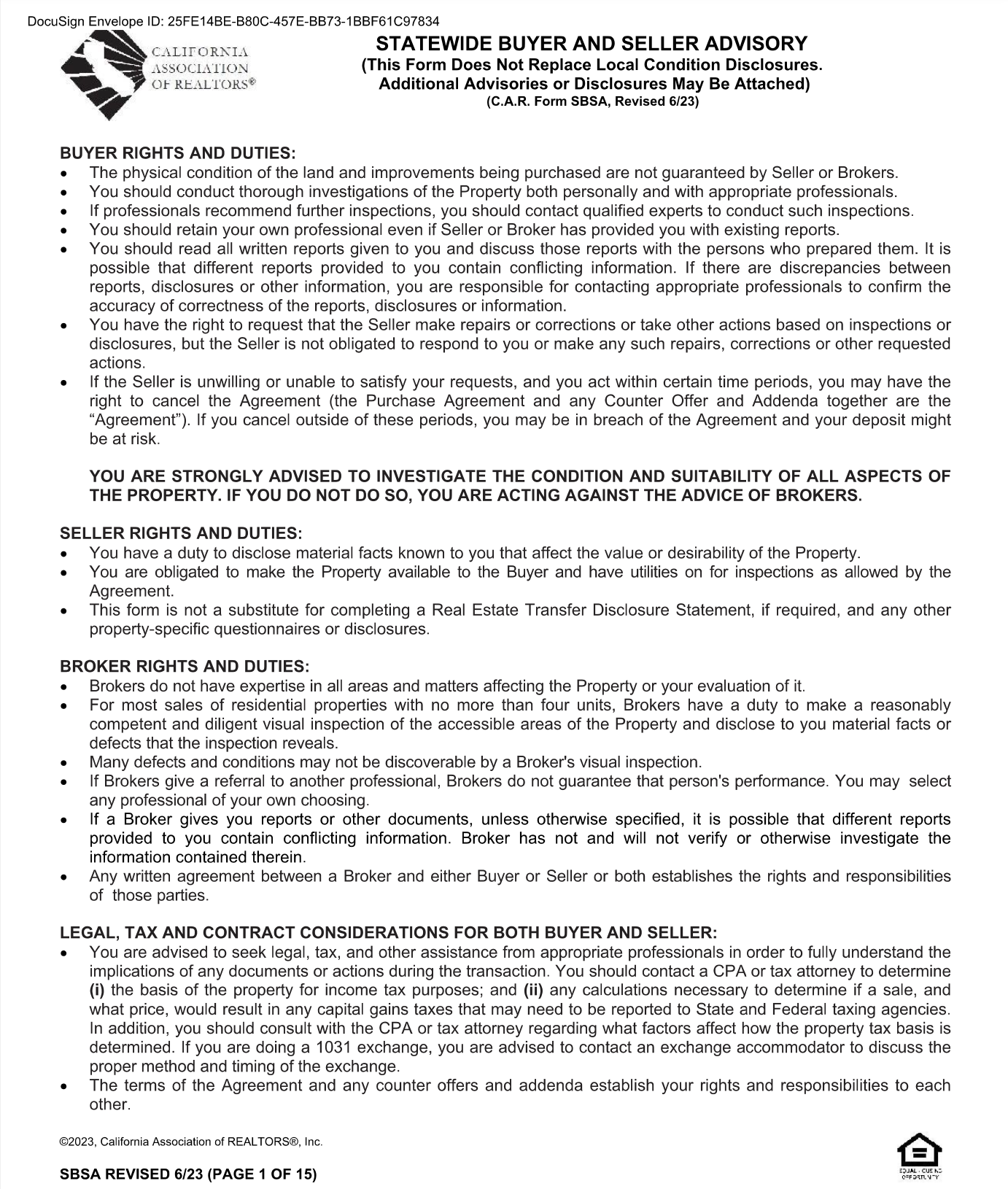

When you find a property that you want to put a bid on, ask to see the disclosures. The purpose of disclosures is for the seller to be transparent about any problems with the house.

Scan through the disclosures to make sure you are aware of any problems. It's important to factor those issues into your purchase price. For example, if the disclosures say that the roof is leaking, you'll need to pay $20,000 for a new roof right away.

These are the forms that I focus on.

The disclosures can look daunting at 150 pages but most of it is standard language that you don’t need to read closely. For example, the Statewide Buyer And Seller Advisory is the same 15 pages for every house.

Now you are ready to decide the purchase price for your bid. Your budget is the amount of your mortgage + your down payment. To decide price, think about whether the house is within your budget and how much of your budget is reasonable to bid on a house.

Here are some things to consider:

Remember that you will need to pay 3% of the purchase price as an initial deposit (aka earnest money deposit) a few days after you have an accepted bid. Double check that you have this cash ready to wire to the escrow agent.

Contingencies generally have the same effect when buying a house. They are favorable to the buyer because they give the buyer an "out" to not buy the house.

Some buyers who are financially secure or highly confident in being able to get financing will waive contingencies to be more appealing to the seller.

The financing contingency means that the contract is contingent on the buyer actually obtaining mortgage financing. If you are not able to get the mortgage, then the financing contingency will remain and you won’t be required to purchase the property.

What's Standard?

As part of your bid, you need to decide on a number of days to remove the financing contingency. This is essentially a deadline by which date you need to have obtained your mortgage commitment from the lender. The standard is 17 days.

I think about this contingency being about me as the borrower. If I were to suddenly get laid off, the lender won't be willing to give me a mortgage anymore. In that case, the financing contingency protects me by allowing me to cancel the contract.

The appraisal contingency relates to the actual value of the property you want to buy. A lender's only recourse if you default on a mortgage is to sell the property, and if the property is worth a lot less than the mortgage, the lender won’t be able to recover all of its money. Therefore, if the property appraises for less than the purchase price, then lender won’t give you the full amount of the mortgage and you won’t be obligated to close.

What's Standard?

You also need to decide on the number of days to remove the appraisal contingency. It’s the deadline by which the third party appraiser needs to provide the appraisal report. Typically, this is also 17 days.

I like to think about this as the “did I overpay” test. Even if the lender approves my application and is comfortable lending to me, if the property appraises at less than the purchase price, the lender won’t give me a mortgage for the full amount and I can cancel the contract.

The inspection contingency gives you a right to investigate the property after singing the contract. You can hire professionals to conduct a general home inspection or specialized inspections for roof, pest, sewer, chimney, foundation, HVAC, and electricity.

If there are issues, you can either request that the seller make repairs or actually have the seller pay you money so you can make the repairs yourself after closing. If you uncover a real deal-breaker issue, you can cancel the agreement.

What's Standard?

The standard is 17 days but you could offer less if you think you can get your inspectors lined up quickly. You could even waive the investigation contingency if you are confident there are no issues with the property.

This is my favorite contingency. A home is the most expensive thing I’ll ever buy, and I want to have the time to make sure there are no hidden problems with the property. Realistically, I’m not going to have the ability to do a thorough investigation of the property before putting down a bid, so I highly recommend keeping this contingency.

When you submit your bid, you could just put together an email and provide the key terms. As an example, this was all the information our broker need to put together the bid.

| Term Sheet | |

|---|---|

| Purchase price | $735,000 |

| Down payment | $250,000 |

| Down payment percentage | 34% |

| Appraisal contingency | Waive |

| Investigation contingency | 10 days |

| Financing contingency | Waive |

| Initial earnest money deposit | $22,050 |