Mortgage approval is the process by which a lender evaluates and officially commits to giving you a mortgage. After getting approval, you'll able to remove your mortgage contingency and close on your house!

You've come a long way in your home buying journey - from prequalifying to finding a home, submitting a bid, and getting your bid accepted, you are almost there! Now it's time to get final approval for the mortgage.

Here is how I handled the mortgage approval process for the home I purchased last year.

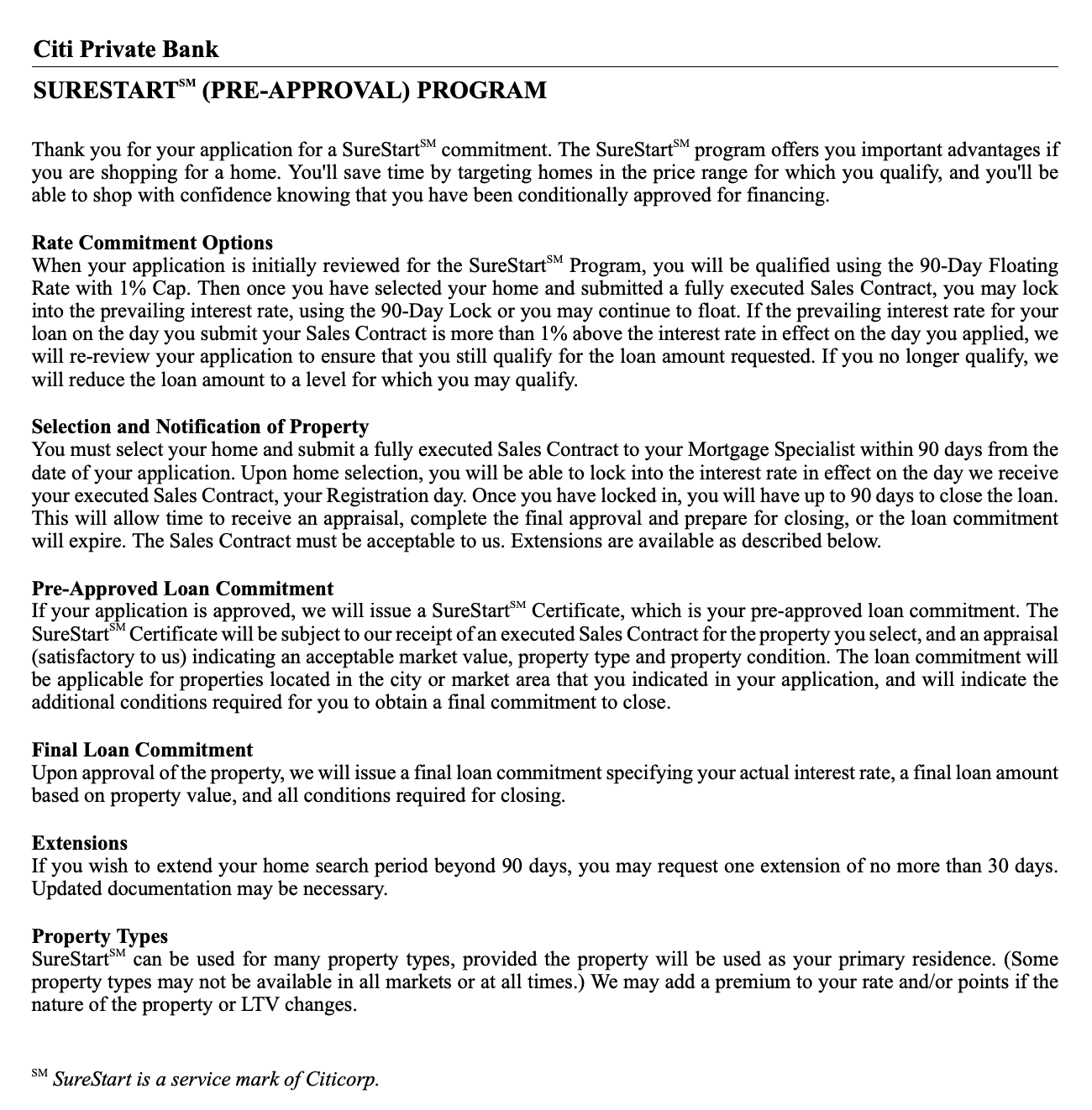

The program overview tells you how to lock in the interest rate for your mortgage.

Here is the overview for the program I used last year with Citibank.

Rate Commitment Options relates to when you lock your interest rate. In the Citibank program, I couldn't lock my interest rate until I had a fully signed contract.

Selection and Notification of Property says that you have to get an accepted offer within 90 days. Once you have gone "under contract", you can lock in your interest rate, but the lock is only good for 90 days. If it takes longer than 90 days to close, you might lose your interest rate.

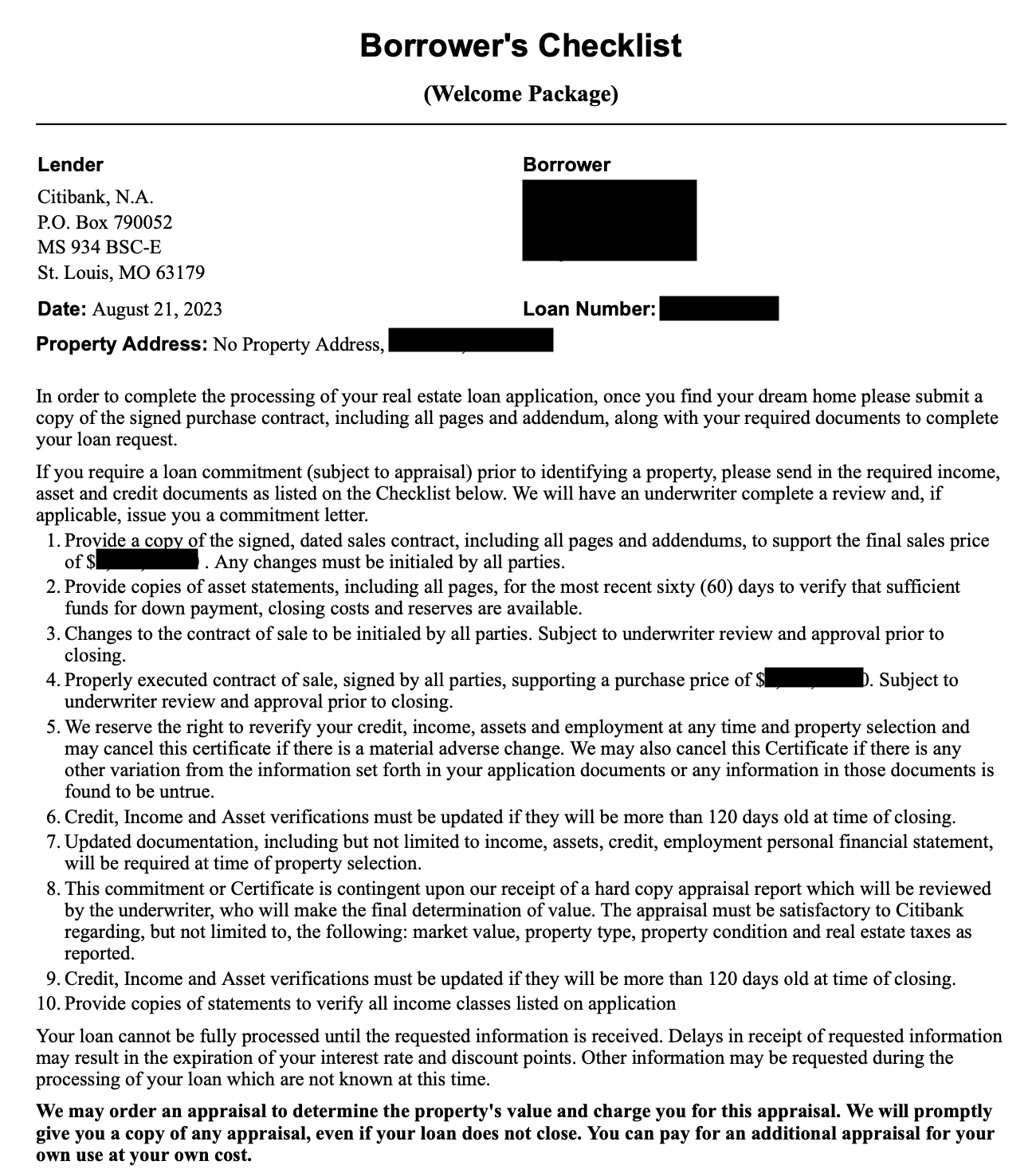

The borrower's checklist is a list of everything you need to provide to the lender.

As soon as you sign the residential purchase agreement, send the contract to the lender so they can start the official loan underwriting and approval process.

If you have signed any amendments reducing the price after an inspection contingency, don't forget to send any amendments to the contract.

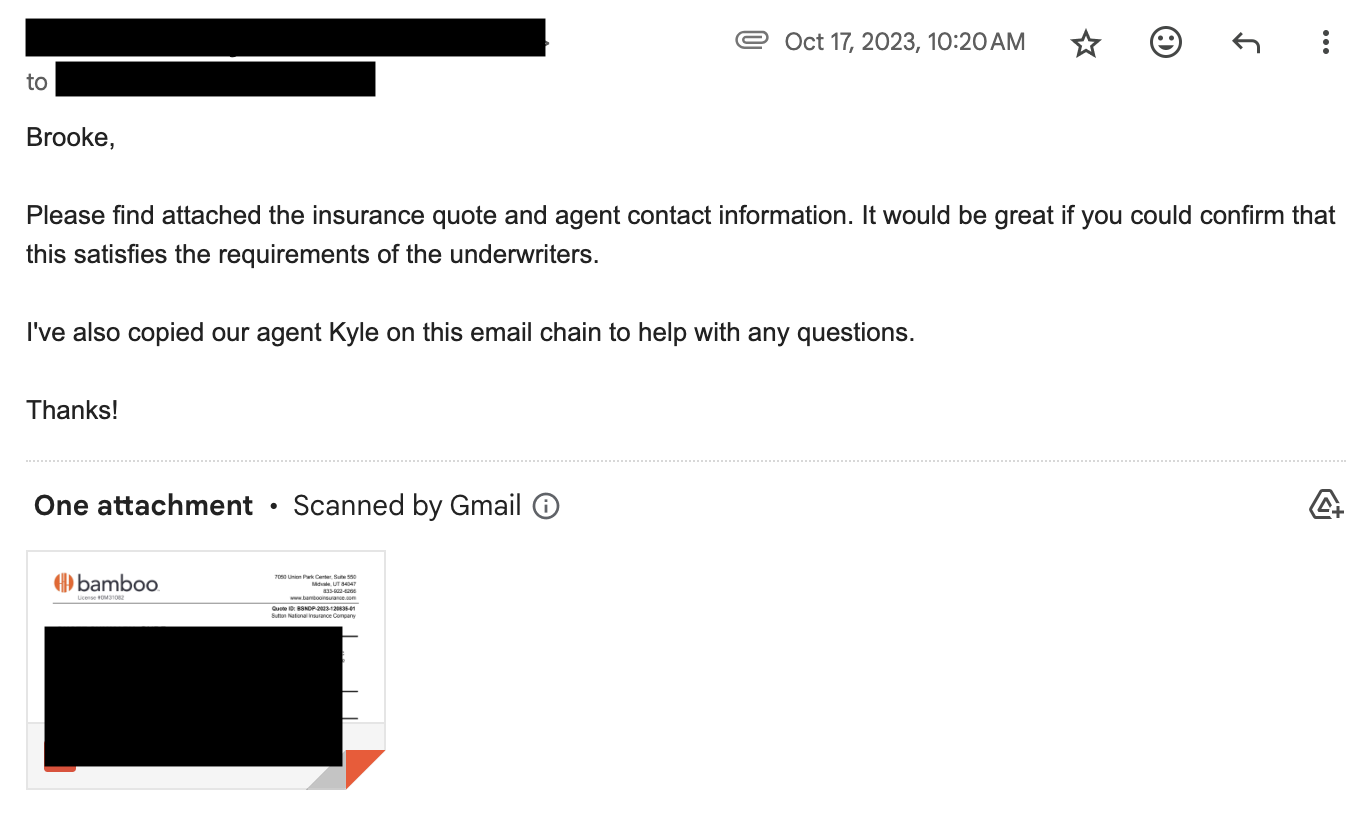

The lender requires you to get home insurance before closing. Get a quote and then introduce the insurance agent to the loan officer.

Try reaching out to your car insurance to see if you can bundle home insurance to get a discount.

You can also work with a broker who will search for the best policy for you.

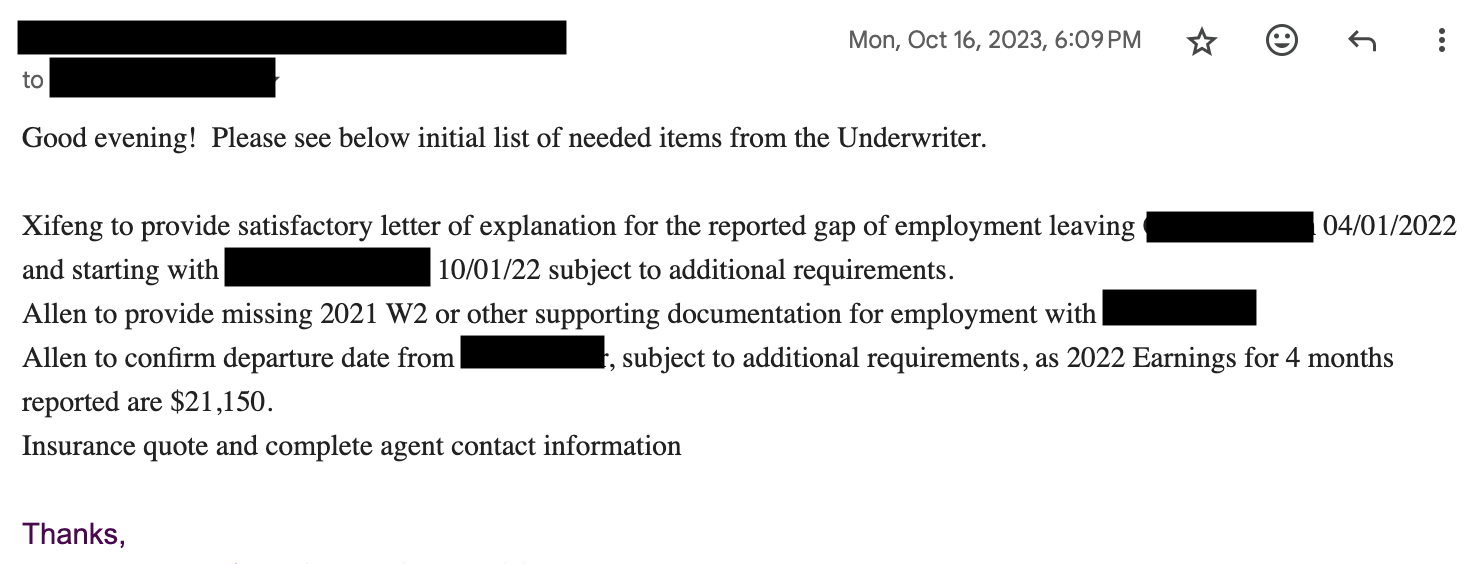

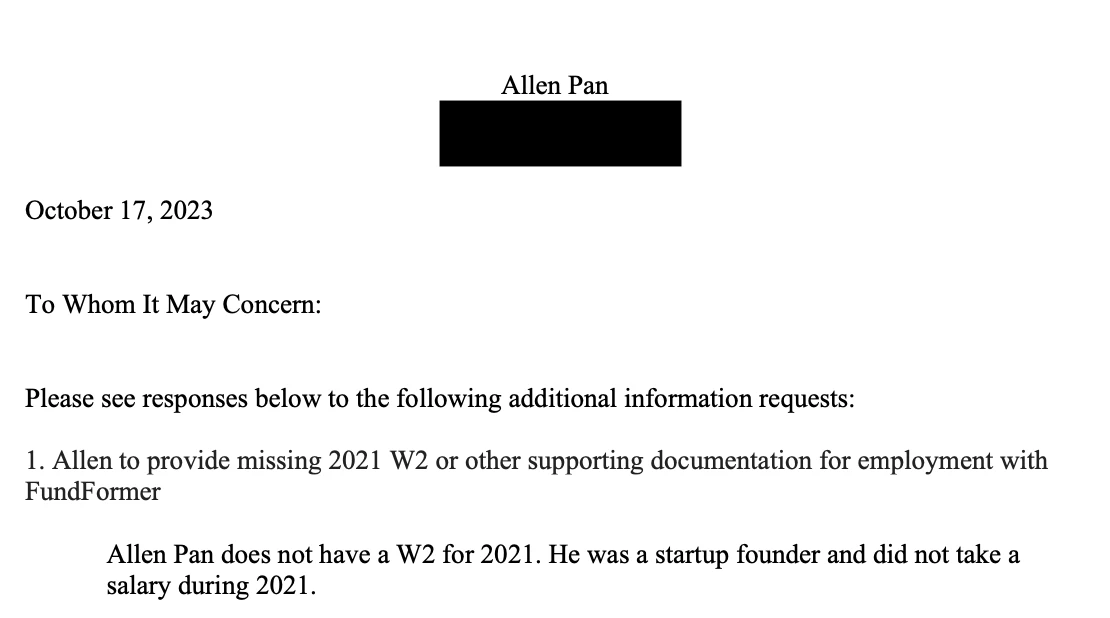

Now that you have the signed contract, the underwriter at the lender is going to request more explanations or documents.

In our case, they asked about a gap in employment, missing W2s, and departure dates.

This is an example of how you can respond to a request for additional explanation.

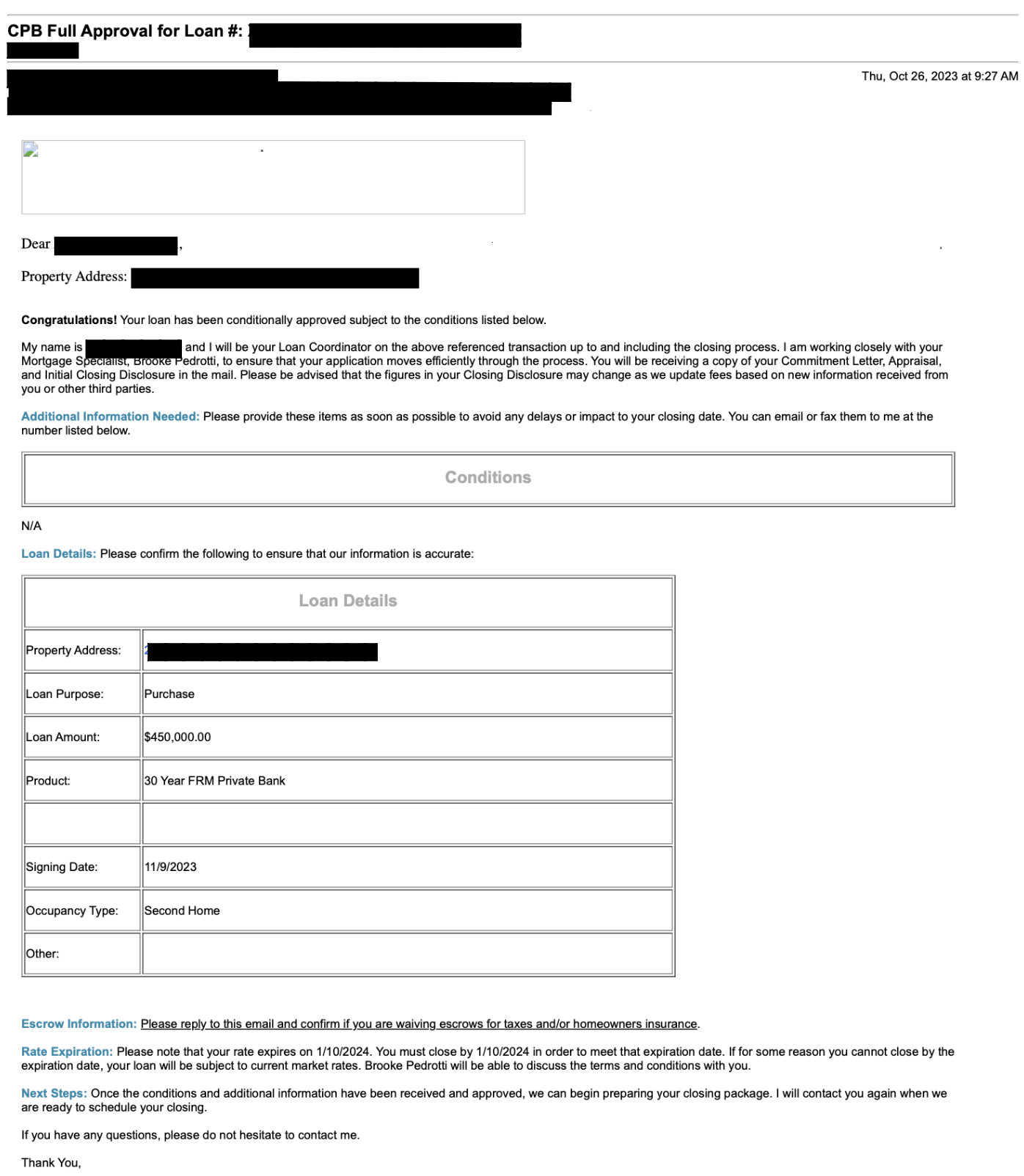

This is what you’ve been waiting for! Now you can remove the mortgage contingency.

This is the email we got confirming full mortgage approval.

Escrow Information was asking whether I want to escrow taxes and home insurance (the lender would collect those expenses as part of my mortgage payment). I chose to waive those escrows because I wanted to handle those myself.

Rate Expiration meant that I had to close by January 9, 2024, which was 90 days after we signed the contract and locked the interest rate on October 10, 2023.