The appraisal contingency is a clause in the residential purchase agreement that allows you to cancel the contract if the property's appraised value is lower than the agreed-upon purchase price.

The appraisal contingency looks at the value of the property you want to buy. If the property appraises for less than the purchase price, then the lender won’t give you the full amount of the mortgage you need to buy the house.

Here is how I handled the appraisal contingency in the house I purchased last year.

Let's take it from the top:

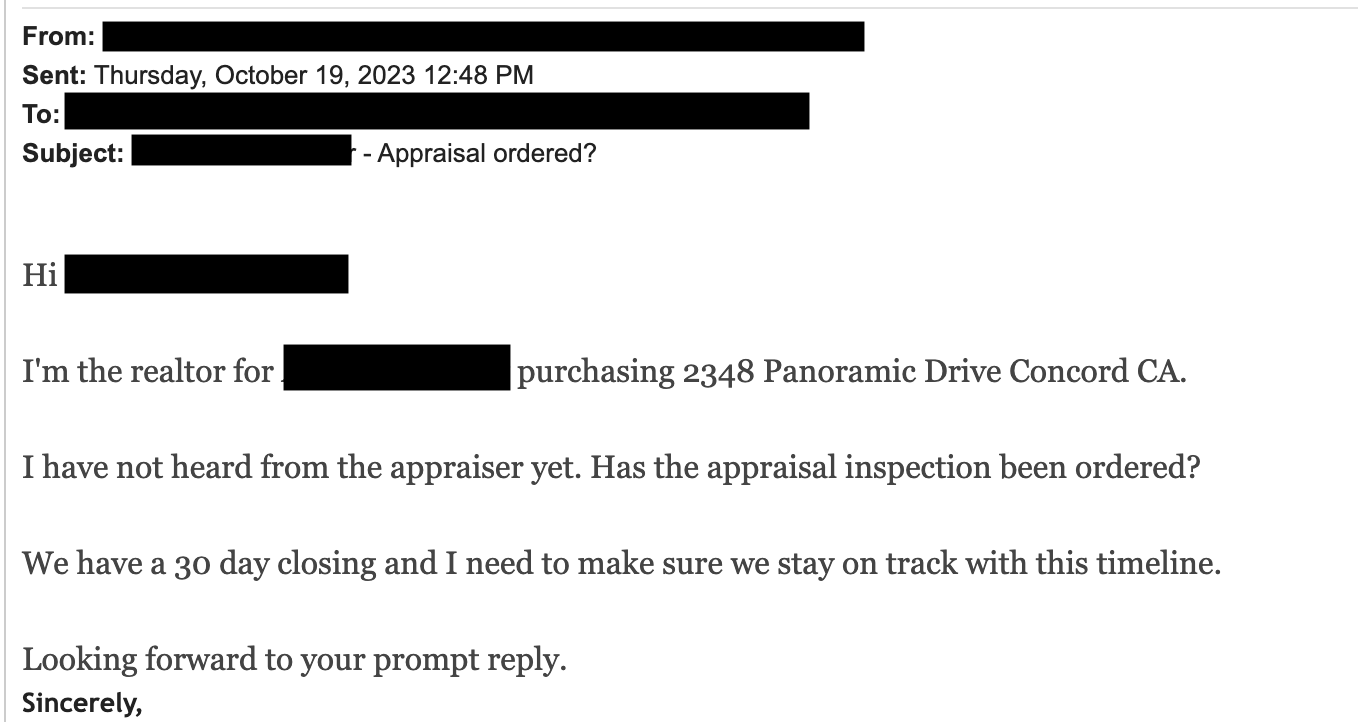

The appraisal is typically ordered by the lender, but if you haven’t heard anything about an appraisal one week after signing, send a check-in email

Here is an example email that you can send. Our contract was signed on October 11 and the check-in email was sent on October 19.

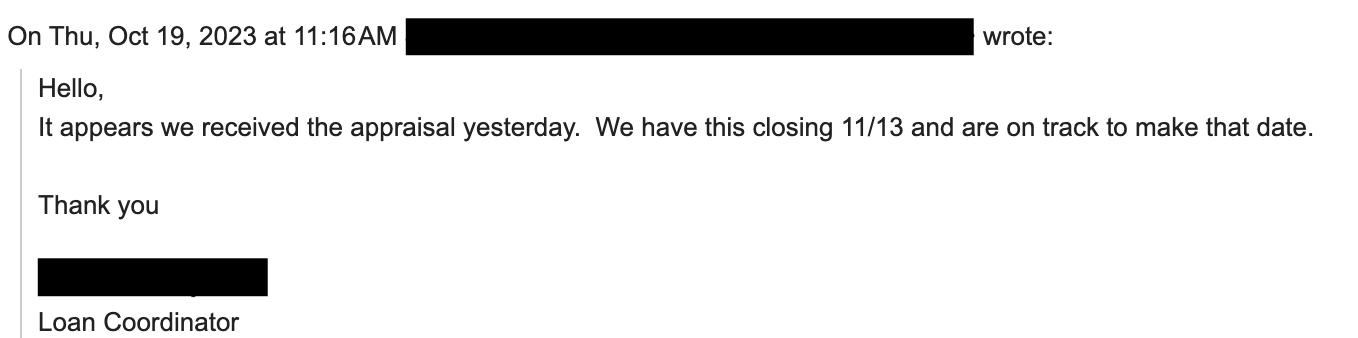

It turns out that the lender had already ordered and received the appraisal.

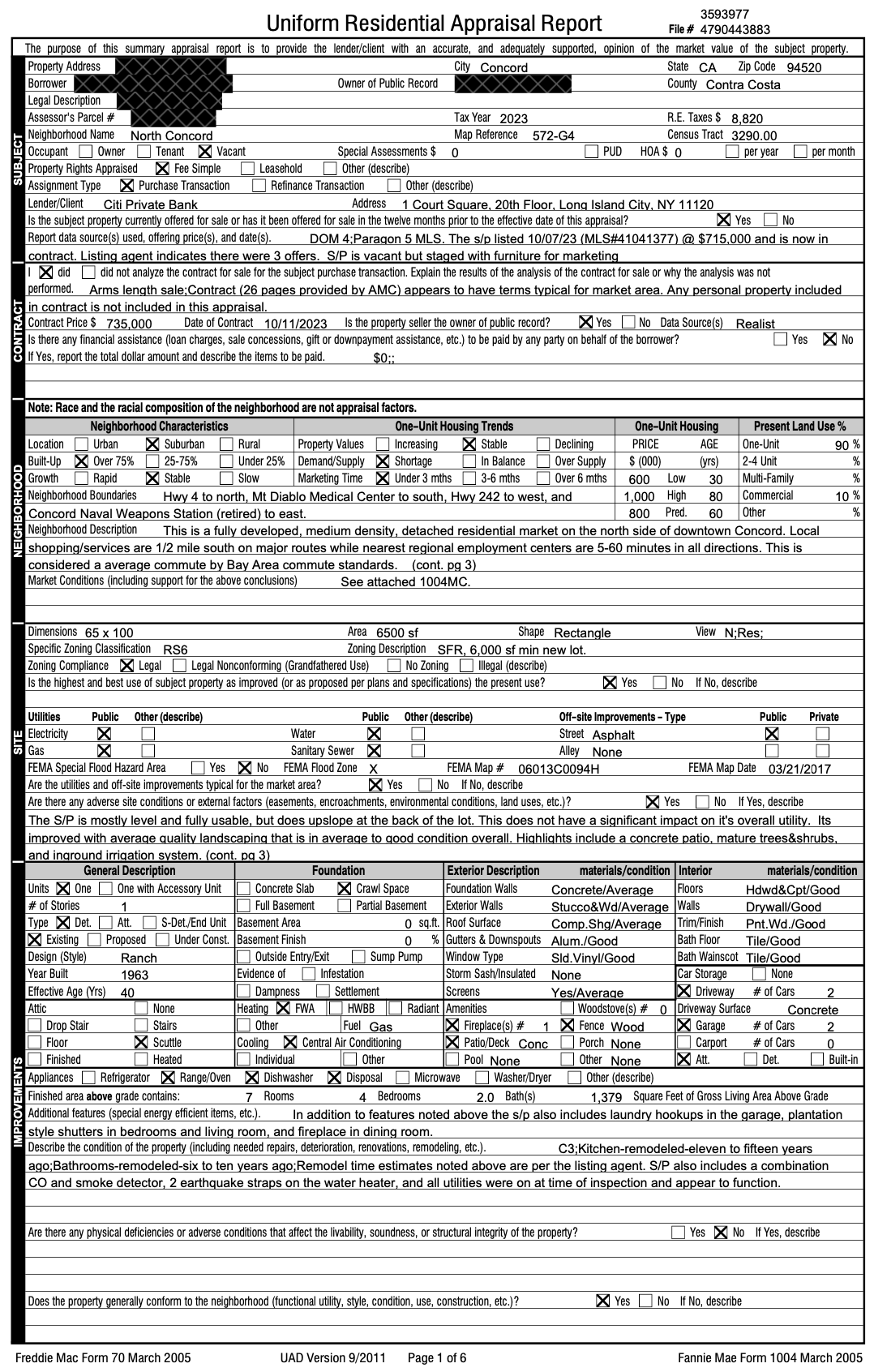

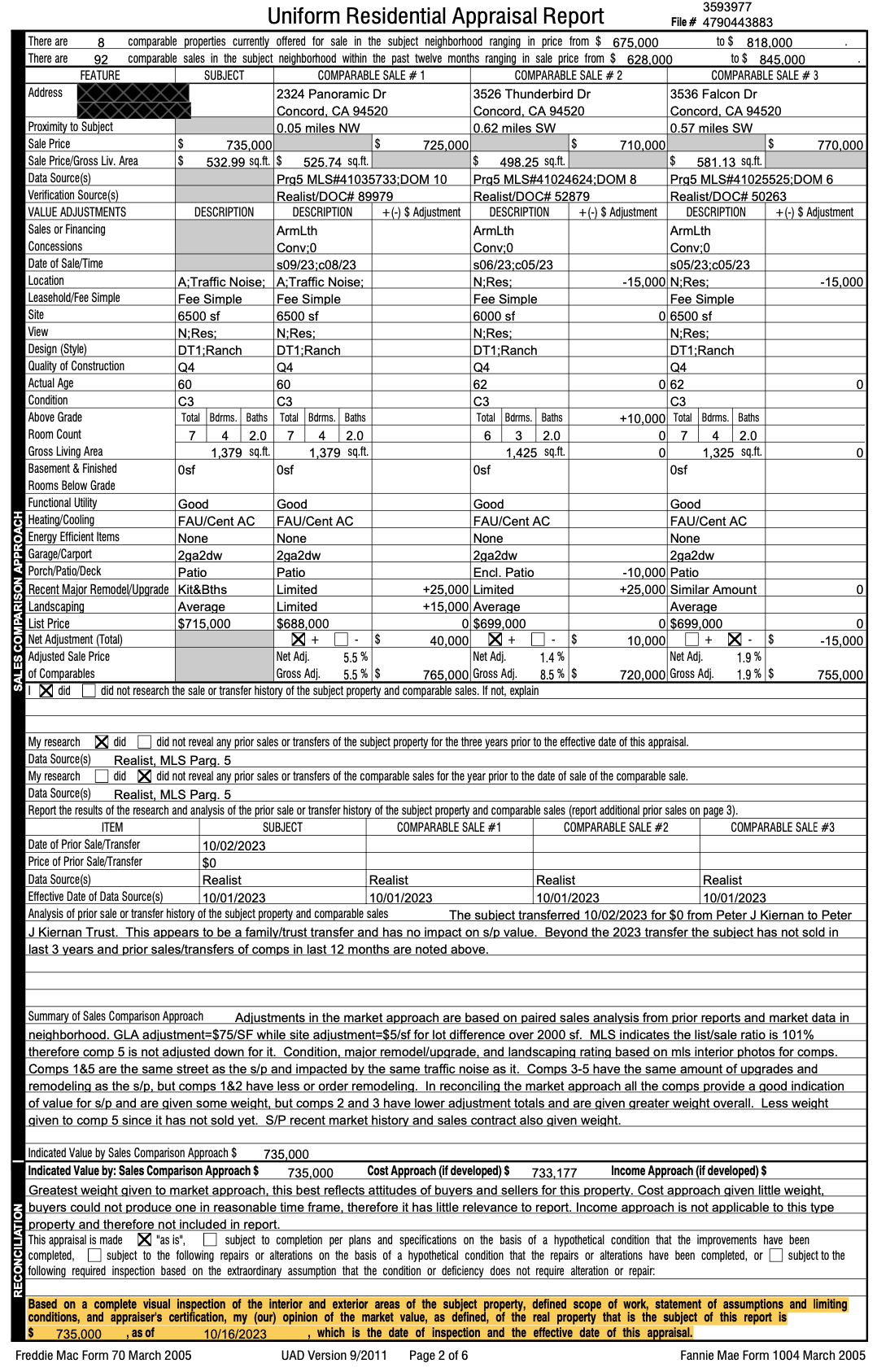

This was our appraisal report. The only number you really care about is the final valuation.

Page 1 describes the property, the contract, the neighborhood, site, and home improvements.

Page 2 describes how the appraiser did an analysis of comparable home sales to arrive at a market valuation of $735,000. It's at the very bottom of page 2.

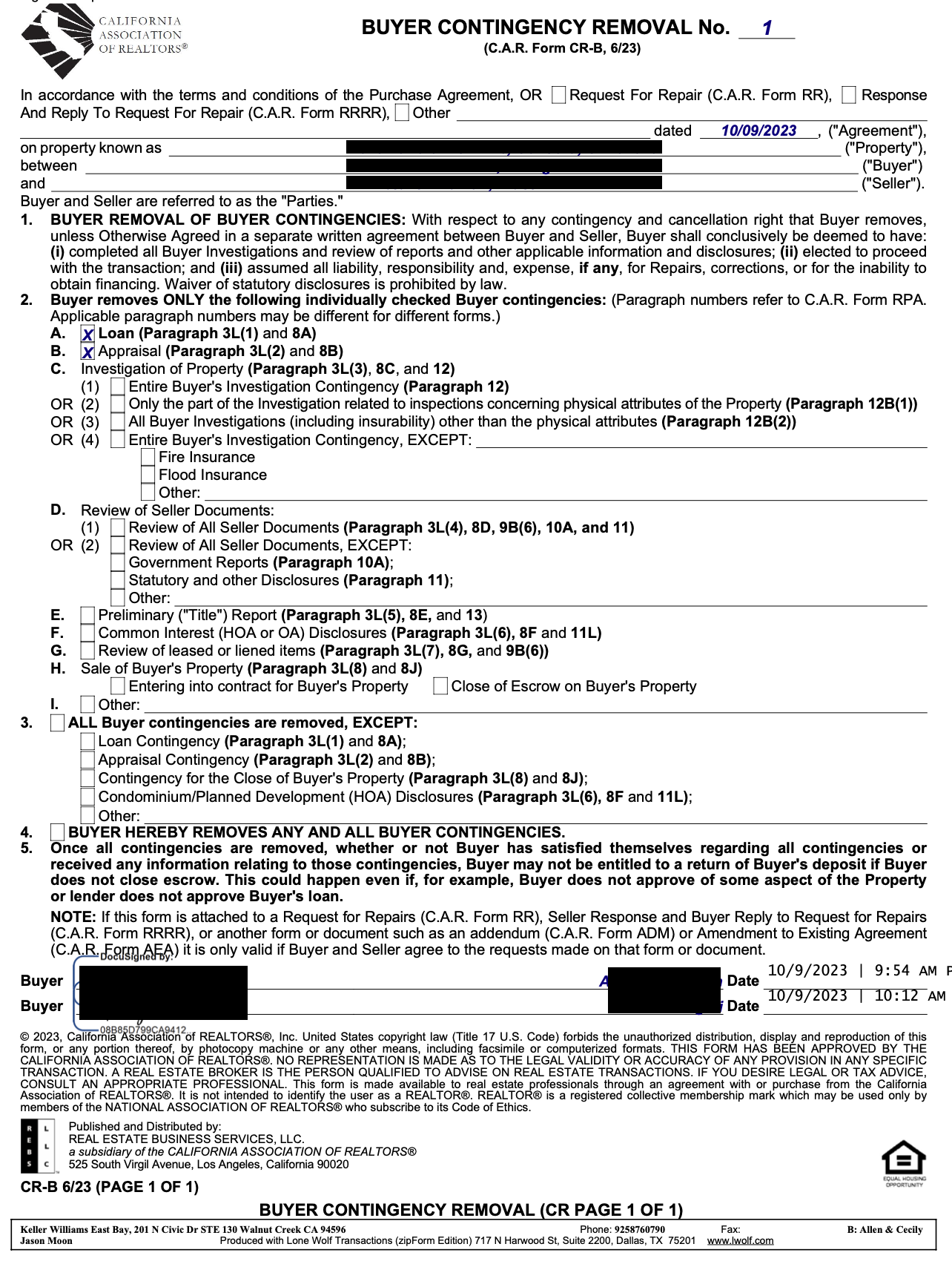

If the appraisal valuation comes in at or above the purchase price, then everything is good and there is nothing else for you to do. You can now remove the appraisal contingency by filling out a contingency removal form.

This is how we filled out an actual contingency removal form.

If the appraisal valuation comes in below the purchase price, there is an opportunity to reduce the purchase price.

But first, just to be comprehensive, there are a couple ways you could challenge the appraisal.

First, you could present additional sales data the appraiser may have overlooked. Personally, I think it's hard to get the appraiser to change the valuation.

Second, you could request a second appraiser, but that might be at your own expense and there is always the chance the second valuation still comes in below purchase price.

Instead of challenging the appraisal, here are some more common options.

You can ask the seller to lower the purchase price to match the appraised value. This is a common approach because it aligns the price with the property's actual market value.

As a compromise, you could also offer to split the difference between the appraised value and the purchase price. In this case, the seller reduces the price and you put in more cash

If you won a competitive bidding process and the seller has a backup bid, you might not be able to convince the seller to reduce price. In this case, you have the option to increase the downpayment to cover the difference between the appraised value and the purchase price.

As an example, if your valuation comes in $5k below the purchase price and you could increase your down payment by $5k.

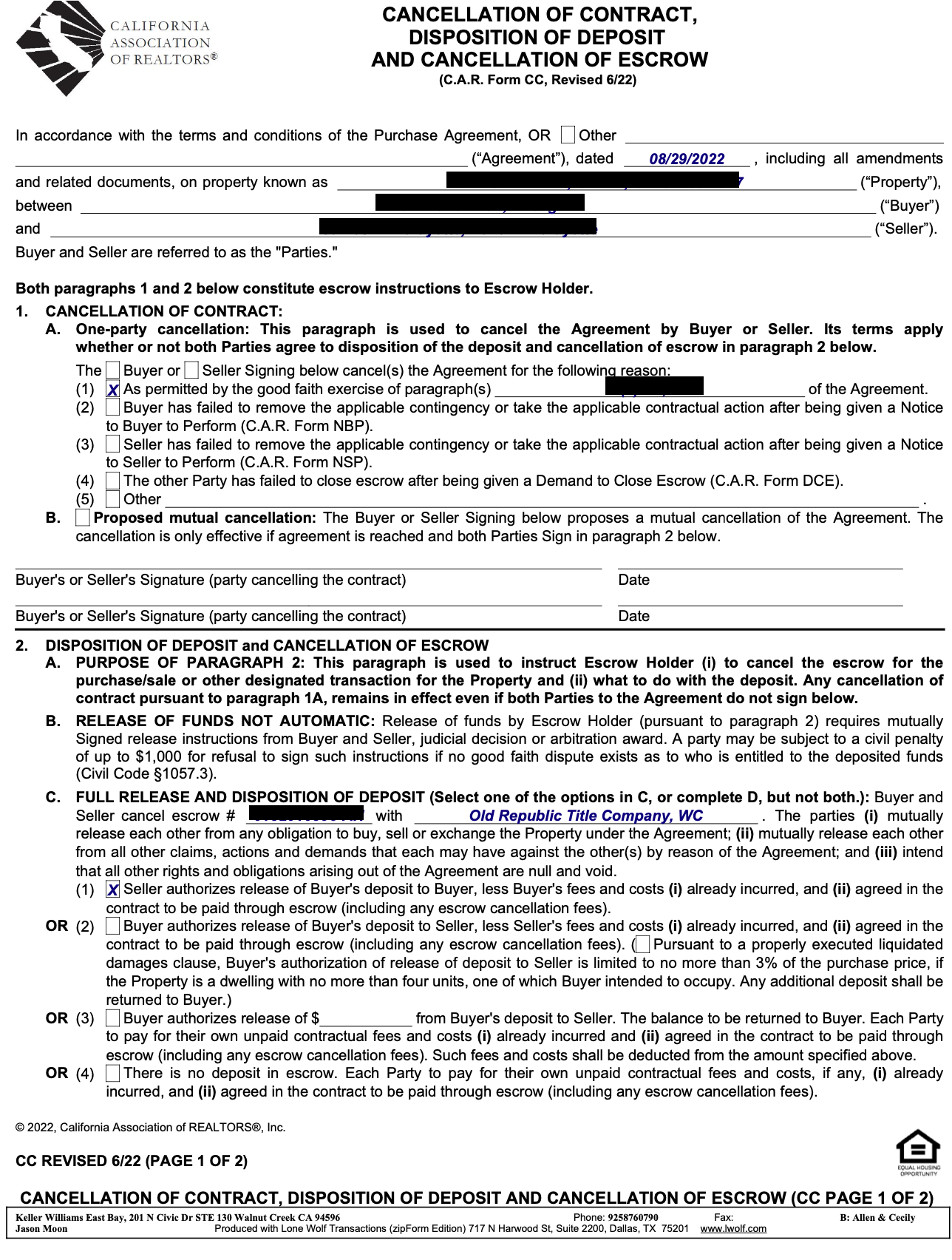

Finally, you can exercise the appraisal contingency in the contract to walk away without losing your earnest money deposit. This might be your best option if renegotiation fails and the property isn't worth the agreed-upon price.

This is an example of how you would fill out the cancellation form.